In spite of the fact that they don’t get much attention in basic economics classes, we live in a world where we are subject to auctions almost constantly. It’s not just getting something on eBay or other auction sites, but it’s how many things are distributed in the public sphere. You can sell Google articles on bandwidth auctions, as one example in the real world. The ads you see on Google are the result of a constant stream of small auctions. Likewise, the automatic price changes for books on Amazon resulted in a computer-driven price of $2,198,177.95 for one book as two robots tried to outbid each other.

Basic Concepts

An auction depends on bids and a market:

- Not everyone values things the same. A lobster dinner looks good to me, but deadly to someone with a shellfish allergy. That final copy of The Flash #123 will complete my comic book collection, so despite being valuable in itself, that comic book has special value to me as a collector.

- Personal valuations change over time. I might eat a second lobster dinner immediately after the first one, but a third lobster is too much to eat right now. Call me next week, please.

- People do not trade unless they feel what they gain is more valuable than what they lose. I want that lobster dinner more than I want the $25 in my pocket. But I want $50 in my pocket more than a lobster in my belly. If I find out I bought crayfish and not lobster, I feel cheated and regret my purchase. This is called buyer’s remorse.

- Auction Theory 101 disallows something that happens in the real world: collusion. Groups of buyers can get together and agree to restrict their bids in some way that’s advantageous to them. The versions of auctions that are taught in economics classes start with the assumption that everyone is making a bid based on their accurate evaluation. Your Auction Theory 102 class will go into game theory and how to collude properly.

Bids have to stop at some point in time, so there is usually a deadline. There can be sealed-bids, where each bidder has a fixed number of bids (usually one) that they traditionally submit in an envelope. Open bid auctions are more lively; the bidders call out their offers until the auctioneer closes the bidding. You can enter and leave the auction at will.

These days, bidders do it online with bid snatcher software that automatically submits a bid that is under a pre-set limit. The usual strategy is to wait until the last possible minute (one second? micro-second? nano-second?) to get in a bid in so short a time slot that no human can type fast enough to beat you.

Types of Auctions

Auctions come in all kinds of flavors, but the basic parts are an offering of something (“I have here a mint-condition first edition of CAPTAIN BILLY’S WHIZBANG, 1919! I start the bidding at $500!”) and bids (“I’ll offer $750 for it. But I would pay up to $1000 for it; maybe I will get lucky!”). The bid can be accepted or rejected. If the bid is accepted, the item changes ownership. Now I get in some strategy here. Should I start with a very low bid and see if I get lucky? Should I start with a medium bid to discourage other bidders? Should I say to heck with it and just throw out my best offer first?

The least interactive auction is the first price sealed bid. The bidders submit sealed bids to the auctioneer, and then the auctioneer opens the bids and picks the winner. This form of auction is used for construction contracting, some military procurement, private-firm procurement, refinancing credit, foreign exchange, and many other goods. The bids are usually complicated things in which the bidder offers to fulfill a contract of some sort in detail. If you’re a Star Trek fan, then this “take it or leave it” approach is how Klingons do business. If you are making a deal with a Klingon, you either drink blood-wine together or shoot it out!

Broadly speaking, there are two styles of processing bids; ascending price (English) and descending price (Dutch).

English Auctions are also known as increasing or ascending price auctions. The auctioneer asks for a starting price, and the bidders increase the price until the item sells or the price offered is not high enough to meet a minimum bid, and the auction fails. This is the form that most of us know. It is how eBay works. Sort of. eBay is more complicated.

Dutch Auctions are also known as descending price auctions. The auctioneer asks for a high starting price, then drops the price lower and lower in steps until the item clears or the auction fails. This form of auction was popular with small retail stores in small American towns in the early 1900s. The items would be placed in the store window with a flip-chart price tag and an announcement that the price would decrease a certain predictable amount, say $1.00, per day until sold. Today, the Dutch auction is hidden in online clearance sales. Instead of looking at the store window on Main street, you get a series of email advertisements at lower and lower prices.

There are various forms of both categories. The Japanese auction is an ascending price auction with levels or tiers. Once you drop out, you cannot re-enter the bidding. For example, if the starting bid is $10, every interested bidder agrees to meet it. They may be required to show that they have at least that much money available, should they win. The auctioneer will then go up a level, say $15; anyone who fails to meet the new level is out and cannot re-enter the bidding, even if they are willing to pay a higher price later. You have a lot of information – the number of other bidders at every level and their exit prices. The auction continues until only one bidder remains.

Obviously, a winner can have buyer’s remorse – the feeling that they paid too much for the item. If you have seen bidding wars on eBay or in real life, you understand how emotions can get mixed up in the heat of the moment.

The solution is Vickrey or second-price auctions. The highest bidder wins, but the price paid is either the second-highest bid or a price between the highest and second-highest bids. The winner cannot be unhappy; he paid less than his bid and won. The losers cannot be unhappy; they all bid less than the winner.

The eBay proxy bid system is a form of second-price auction. A variant of a Vickrey auction, named generalized second-price auction is used in Google’s and Yahoo!’s online advertisement programs. The computer runs hundreds or thousands of auctions for the on-line adverting slots they sell. The auctioneer will probably like the idea of a bid between the highest and second-highest bids since it results in a little more profit.

Auction Database Schema

What should the skeleton of a database schema for a general auction look like? Let’s start with the bidders and a simple skeleton.

|

1 2 3 |

CREATE TABLE Bidders (bidder_id INTEGER NOT NULL PRIMARY KEY, ...) |

When logging in an item for an auction, you need to identify the item and get a starting bid amount. The minimum bid is also called the reserve amount. If there is no bid, equal to or greater than that amount, the auction is void.

|

1 2 3 4 5 6 7 |

CREATE TABLE Items (item_id CHAR(15) NOT NULL PRIMARY KEY, item_name VARCHAR(25) NOT NULL, initial_bid_amt DECIMAL (12,2) NOT NULL CHECK(initial_bid_amt >= 0.00), minimum_bid_amt DECIMAL (12,2) NOT NULL CHECK(minimum_bid_amt >= 0.00)); |

A bid must be timestamped, and the bid amounts have to increase over time.

|

1 2 3 4 5 6 7 8 9 10 |

CREATE TABLE Bids (item_id CHAR(15) NOT NULL REFERENCES Items (item_id) ON DELETE CASCADE,bidder_id INTEGER NOT NULL REFERENCES Bidders (bidder_id), bid_timestamp TIMESTAMP(0) DEFAULT CURRENT_TIMESTAMP NOT NULL, bid_amt DECIMAL (12,2) NOT NULL CHECK(bid_amt >= 0.00), PRIMARY KEY (item_id, bidder_id, bid_timestamp) ); |

An item can be pulled from the auction, so the DDL should cascade and remove the bids when that happens. A bid can be pulled from the Bids table, but you have an auction as long as there’s at least one bid left the system.

Auctions are good for everyone because:

1) the seller gets compensation for something he might have otherwise discarded.

2) the buyer receives something he wants for the price that he’s agreed upon.

3) the item is assigned to the buyer who objectively wants it the most, and therefore you can assume this is the optimal use of the item.

Another allocation method would be by a raffle among the bidders. This might work if the sale of raffle tickets gives the seller a return equal to or in excess of the item’s value. However, for the economy as a whole, there’s no guarantee the item will wind up with the person who wants it the most. Everyone who has failed to win the lottery resents the winners and is dissatisfied with the fact that they didn’t get the prize. I’ve never quite figured out why anyone would think the universe owes them a winning lottery ticket, but a lot of people do.

Fair Division by Auction

So far, I’ve talked about using an auction to get a buyer and a seller together with one item. However, this technique is much more general. Imagine that Uncle Scrooge McDuck has died and left his estate to his heirs. Some of his estate is in the form of money, which is pretty easy to divide up, and several goods which cannot be split up. Unfortunately, one solution is to sell everything and then make sure that the entire estate is expressed in money. This is unfortunate because the heirs might actually want to keep something without having to monetize it. We need a different procedure.

The Knaster Inheritance Procedure (KIP) is named after Bronislaw Knaster. This is an auction scheme designed for an estate with many heirs, assuming that each heir has a large amount of cash at their disposal. The basic idea is that you auction all of the indivisible property in the estate to the heirs (bidders) and then adjust what the heirs think is a fair value.

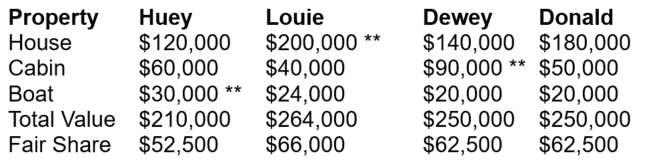

This is easier to see with an actual example. Suppose that Huey, Louie, Dewey and Donald are splitting up a house, a cabin, and a boat. You get bonus points if you know the actual names of Donald Duck’s nephews (spoiler: Dewey is actually “Deuteronomy”). They then give bids for each item, as shown below.

To divide up more than one item using the Knaster Inheritance procedure, you include two more rows: Total Value and Fair Share. The total value is the sum of that person’s bids, and the fair share is the percentage multiple of the total value.

In this example, Huey’s total value = $210,000. His fair share is $210,000 × 0.25 = $52,500.

Each item is given to the person with the highest bid, shown by ** in the chart. Louie gets the house, Dewey gets the cabin, and Huey gets the boat. Poor old Uncle Donald gets nothing. Here’s where the fair share comes into play. Remember that each person expects to get their fair share. Consider them one by one.

- Huey gets the boat, which he valued at $30,000. Since his fair share is $52,500, he then expects the difference in cash: $22,500.

- Louie gets the house, which he valued at $200,000. Notice that his fair share is lower than what he valued the house for. Thus, he expects to pay back the difference, which is $134,000.

- Dewey gets the cabin, which he valued at $90,000. Again, this is higher than His fair share, so he expects to pay back the difference: $27,500.

- Donald receives no property because he didn’t win any of the bids. Thus, he expects to get his fair share in cash: $62,500.

At this point, all four participants are getting what they believe is their fair share.

Notice that Louie and Dewey contribute to the kitty, while Huey and Donald are awarded money from it. Thus, our surplus is $134,000 + $27,500 − $22,500 − $62,500 = $76,500. This will then be divided among the four. Therefore, each duck gets an additional $76,500 × 0.25 = $19,125.

Thus, the final outcomes are:

- Huey gets the boat, $22,500 for the fair share adjustment, and $19,125 from the surplus.

- Louie gets the house and $19,125 from the surplus. He also has to pay $134,000 for the fair share adjustment.

- Dewey gets the cabin and $19,125 from the surplus. He also has to pay $27,500 for the fair share adjustment.

- Donald receives his fair share of $62,500 and $19,125 from the surplus.

In fairness, these calculations are probably better done with the spreadsheet than in a database. There are trade-offs with this procedure. On the good side, it can be extended to any number of items among any number of participants. Bids are done in secret and only once. The downside is that the amount of money involved can get pretty big. It’s also possible that one bidder who is willing to pay enough to beat everybody else, he can inherit everything. This might not be a downside if only one of the heirs to the estate really cares about the property and everybody else is just in it for the money.

Cheating

The seller wants to get the highest price for his goods, obviously. The fact or illusion of competition works in his favor, so the seller has an incentive to have shills bid up the price. At English auctions, the auctioneer himself pretends to hear bids (his incentive is that he gets paid by a percentage of sales); this is sometimes referred to as chandelier or rafter bids.

Then there is the outright shill bid. You get your fellow co-conspirator to bid on the item, even though they have no intention of buying it. One way to discourage shill bidding is to set a reserve price, so the seller is guaranteed a guaranteed minimum return. Another way is to detect shills is through the bid patterns. Typically, the shill increments the price by only small amounts, so as not to discourage a genuinely interested bidder from staying in the auction. The auction rules can require a minimum bid increment to discourage this behavior.

Another way to cheat is just outright collusion. The bidders get together before the auction and decide what the price will be. This has been done in several high-profile government auctions and was part of the storyline in John Steinbeck’s “The Pearl” short story.

The Bottom Line

Honesty seems to be the best general strategy. Do not overbid what you think the item is worth to you. If you pay your evaluation of the item, then you just made a routine purchase. If you pay less than your assessment, then you got a bonus. If you lose, then you still have your money.

This document contains proprietary information and is protected by copyright law.

Copyright © 2026 Red Gate Software Limited. All rights reserved

Load comments